Investing is a key way to grow your money and achieve your financial goals. However, many people avoid investing because they lack the time or skill. Fortunately, platforms like Betterment help make investing easy for anyone.

Betterment is a robo-advisor that can manage your portfolio at a minimal cost. In fact, the platform lets you start investing with $0. With Betterment, you don’t trade individual stocks or mutual funds that can be risky and have high fees.

Instead, you invest in a bucket of Exchange Traded Funds (ETFs) index funds that fit your specific goals.

Table of Contents

What is Betterment?

Betterment launched in 2008 and is the most established player in the robo-advisor space. Today, the advisor manages over $21 billion in assets and has 500,000+ clients.

You can open taxable, traditional individual retirement accounts (IRAs) and Roth IRAs.

A decade ago, investors had to pay a hefty fee for managed portfolios. The “free” option was (and continues to be) investing on your own.

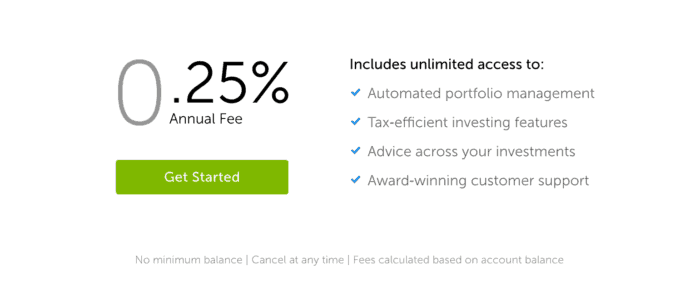

Betterment can manage your portfolio for less than a traditional advisor. While most advisors charge at least one percent, the Betterment annual advisory fee is only 0.25 percent.

You can keep your investing fees and portfolio risk low by investing with passive index funds. When you pay fewer fees, you’ll have more cash to invest.

Betterment also offers these additional features:

- Access to financial advisors

- Fee-free checking accounts

- Interest-bearing cash management accounts

If you’re looking for other features, read our guide on the top Betterment alternatives to find a suitable option.

How Betterment Works

Betterment invests in multiple US and foreign stock and bond asset classes using index fund exchange-traded funds (ETFs). Index funds have low fees so you can invest more cash and have instant diversification.

One of the main reasons to use Betterment is that it has fully-automated portfolios. You can invest in stock and bond index ETFs that fit your age and investing goals, including:

- Retirement

- General investing (i.e., generate passive income)

- Saving for a major purchase

- Building a cash safety net

Betterment will recommend different stock and bond asset allocations for each of your goals. For example, you will mostly invest in stocks if you have several decades until retirement.

Alternately, your cash safety net will hold more bond funds than stock funds since they are less risky.

As you invest new cash, your portfolio is automatically rebalanced. Free tax-loss harvesting comes with every account to help reduce your taxable income. These perks remove some of the hassles that come with investing.

You can open multiple accounts with different goals. These accounts can help you plan for short-term and long-term goals.

Betterment at a Glance

| Info | Data |

|---|---|

| Minimum Investment | ✓ $0 |

| Account Types | ✓ Retirement | Trusts | Taxable | Joint |

| Management Fee | ✓ 0.25% / yr. (0.4% for $100K) |

| Features | ✓ 401(k) assistance |

| ✓ Tax loss harvesting | |

| ✓ Portfolio rebalancing | |

| ✓ Auto deposits (weekly, bi-weekly, monthly) | |

| ✓ Advice from real humans | |

| ✓ Socially responsible investing | |

| ✓ Fractional shares | |

| ✓ Cust. Svc.: Phone, live chat, email | |

| Get Started | Sign Up Now |

If you’re a new investor, this hands-on approach helps you avoid common investing mistakes.

How to Open an Account

Here’s a step-by-step at what it looks like to open an account with Betterment.

1. Choose a Taxable or Retirement Account

First, you will enter your email address and personal tax details. Then, you decide if you want to open a taxable account or an IRA.

2. Take an Investor Quiz

The next step is completing the investor quiz. In 15 minutes or less, you’ll answer several questions about your investing goals.

Once you finish the quiz, you will see your personal investment plan. Your plan will list which ETFs are viable investment opportunities for you.

3. Fund Your Account

The final step is funding your investment account from a linked bank account. It takes up to two days to transfers funds. Betterment invests the cash as soon as it arrives in your account.

There are no trade commissions to buy or sell funds. You can invest as little as $10 at a time. Since Betterment buys fractional ETF shares, you won’t have idle cash sitting in your investment account.

Setting up recurring deposits lets you invest regularly. Additionally, Betterment rebalances your asset allocation with each new investment.

Investment Philosophy

Betterment uses an approach that is similar to the buy-and-hold investing strategy. The app focuses on your long-term goals as opposed to trading individual stocks.

This goals-based strategy allows you to invest in US as well as foreign stock and bond index ETFs.

These are some of the stock index ETFs you can invest in:

- VTI – Vanguard Total Stock Market ETF

- VTV – Vanguard US Large-Cap Value Index ETF

- VOE – Vanguard US Mid-Cap Value Index ETF

- VBR – Vanguard US Small-Cap Value Index ETF

- VEA – Vanguard Europe Pacific (EAFE) ETF

- VWO – Vanguard Emerging Markets ETF

You can also invest in these bond index funds:

- SHV – iShares Short-Term Treasury Bond Index ETF

- VTIP – Vanguard Short-term Inflation-Protected Treasury Bond Index ET

- BND – Vanguard US Total Bond Market Index ETF

- MUB – iShares National AMT-Free Muni Bond Index ETF

- LQD – iShares Corporate Bond Index ETF

- BNDX – Vanguard Total International Bond Index ETF

- VWOB – Vanguard Emerging Markets Government Bond Index ETF

Betterment lets you invest in most areas of the stock market. It also allows you to limit your downside risk since the best assets can change from year to year.

Younger investors with a higher risk tolerance will mostly invest in stock funds. For example, you may hold 90 percent in stock funds and ten percent in bond funds at age 20.

As you near retirement, you might only have 60 percent in stocks. The Betterment auto-adjust tool buys more bonds and fewer stocks as you age.

Advanced Investing Strategies

Betterment gives you access to advanced investing strategies that can help you achieve your goals. Like the core portfolios, these plans only invest in ETFs. However, these options may not beat the overall stock market.

Socially Responsible Investing

Index funds are an effortless way to earn passive income, but some funds may invest in companies that don’t align with your values. This is why socially responsible investing (SRI) is a growing trend.

When possible, Betterment avoids funds with poor environmental, social, or corporate governance scores.

Goldman Sachs Smart Beta

The Goldman Sachs Smart Beta plan is for investors with a higher risk tolerance. While this strategy is Betterment’s most aggressive strategy, it strives to keep volatility low.

You can invest in alternative assets like real estate with Smart Beta. Keep in mind that real estate index funds may perform differently than stocks and bonds.

BlackRock Target Income

The BlackRock Target Income portfolio only invests in bonds. This low-risk option can be ideal for retirees wanting a fixed income.

Account Types

It’s possible to have taxable and retirement accounts with Betterment, including:

- Single taxable accounts

- Joint taxable accounts

- Traditional IRAs

- Roth IRAs

- Rollover IRAs

- SEP IRAs

- Inherited IRAs

- Trust IRAs

It is free to open taxable and retirement accounts with Betterment. Other online brokers may require a $500 balance to open an IRA, but Betterment doesn’t require an initial deposit to open an account.

Read our analysis of ways to invest $500 or less to identify those options.

Having multiple accounts unlocks tax-coordinated investing. This perk improves your tax-efficiency and keeps your tax liability low.

Additional Features

Betterment offers several exciting features to help plan for your short-term and long-term goals. You can also open bank accounts for investing and saving.

Retirement

Most people invest to save for retirement but have a hard time planning for their golden years. Betterment’s tools make retirement planning easier.

Retirement Income: This tool projects your monthly retirement spending. You can schedule auto-withdrawals to avoid outliving your savings. Decumulation during retirement can be tricky to balance, but this tool helps

RetireGuide™: This feature differentiates Betterment from other robo-advisors. RetireGuide™ provides you with personalized retirement planning advice based on your goals.

RetireGuide™ will:

- Evaluate income when you retire (based on your current investments)

- Make plans based on the availability of Social Security

- Determine how much you should save each year

This feature also lets you evaluate your entire retirement picture by including your 401(k) plan and other external accounts. Seeing the current balance of your taxable and non-taxable accounts shows your total net worth.

Ultimately, this tool provides advice on what you need to save and where to invest it across your entire portfolio.

SmartDeposit: Do you like to invest money throughout the month? That is the premise behind SmartDeposit. SmartDeposit allows you to invest money once your bank account reaches a certain balance.

Tax-Saving Strategies

Other investing apps only offer traditional or Roth IRAs to reduce your investment taxes.

With Betterment, you get several built-in benefits that can reduce your taxable income from investing. Unless you only invest with a Roth IRA, most passive income is taxable. Paying fewer taxes means you have extra cash to invest and you can earn more compound interest.

Charitable Giving: It’s possible to donate directly to various charities from your account. Betterment will also let you see your potential tax savings. However, this option is only available for long-term gains.

Tax-Coordinated Portfolio: This exciting feature helps Betterment make tax-efficient investments to boost your after-tax performance. For example, Betterment may hold more bonds in your IRA because they earn more taxable income than stocks. Your taxable account might have more stocks as a result.

Bear in mind that this feature only works with Betterment accounts. While you can sync external accounts for investment reviews, this data doesn’t influence the asset allocation Betterment chooses for you.

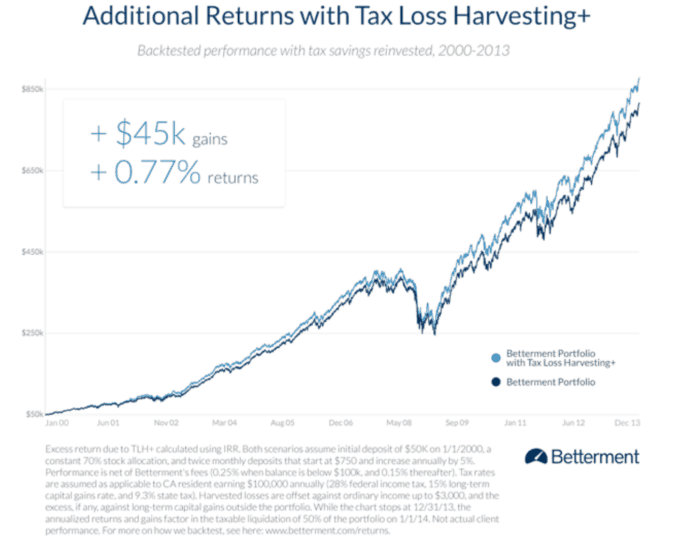

Tax-Loss Harvesting+: The robo-advisor can sell funds for losses to offset your taxable gains. According to Betterment, you might be able to offset up to $3,000 in ordinary taxable income each year.

Personal Support

Live Support: Betterment offers phone and chat support five days a week. You can ask questions about setting goals or navigating the platform. However, the support team cannot provide personal advice.

Premium plan members get unlimited phone access to CFP professionals. You must have at least $100,000 with Betterment to qualify for Premium.

Investment Review: Betterment created this feature to analyze and score your outside investments based on four areas: investment accounts, tax savings, fees, and risk exposure.

The Investment Review feature is free to use. It is a great way to ensure your investments are in shape and that you’re not missing any opportunities.

Advice Packages: It’s possible to schedule financial planning sessions when you need them. You can plan for major life events or get an in-depth portfolio review. These one-time advice calls start at $199 and last 45 minutes.

On-demand financial advisor access: Having at least $100,000 with Betterment gives you complimentary access to certified financial planners. Keep in mind you will need to upgrade to the Premium pricing plan to enjoy this perk.

Cash Reserve

Most bank accounts are notorious for their low interest rates. If you want your spare cash to work harder, Betterment Cash Reserve is an option.

Betterment Cash Reserve is an FDIC-insured product and offers an APY of up to .10 percent. This is one of the highest rates in the market and offers FDIC insurance of up to $1,000,000.

Most online banks only let you make a maximum of six withdrawals each month. Betterment lets you make unlimited withdrawals.

Married couples can open a joint Cash Reserve account and get up to $2,000,000 in FDIC insurance.

Like Betterment’s investing options, it’s free to open a Cash Reserve account. You must make an initial deposit of at least $10, but you do not need to maintain a minimum account balance.

Betterment Checking

There is also a free FDIC-insured checking product up to $250,000 called Betterment Checking. You might pair this product with the Cash Reserve feature to sweep money between accounts.

This feature has no minimum balance requirement or fees. You also get a free Visa debit card for local and online shopping. A fun new feature the advisor has added to the debit card is the ability to earn cash back on your shopping when you use the card.

Offers are personalized on your shopping history and there is no minimum to redeem rewards. They automatically apply earnings to your checking account balance.

Betterment reimburses fees at any ATM that accepts Visa, accounting for roughly 2.8 million spots worldwide. However, there is a one percent fee on all foreign transactions. Instead of looking for an in-network ATM, you can quickly get cash as you need it.

In addition to enrolling in direct deposit, you can deposit checks from your mobile device. The app is available for Android and iOS devices and lets you access your investment accounts.

Instant money transfers are available with Zelle and other apps such as Venmo and Cash App.

Despite the many free features, online bill pay and paper checks are not available. Betterment is exploring adding these features in the future. In the meantime, you can schedule bill payments through the merchant’s website.

Betterment also plans to offer a joint checking account. For now, you and your spouse can open separate accounts.

Fees and Pricing

Betterment has low fees that are competitive with most robo-advisors.

Annual fees for your investment account are either 0.25 percent or 0.40 percent. If your investment account has a $0 balance, you do not pay a fee. Additionally, you don’t pay any fees if you only open a checking or cash reserve account.

There are no trade commissions to buy or sell ETFs with Betterment.

You will pay annual ETF expense ratios between .07 percent and .12 percent for most funds. The fund manager retains this fee from your dividends.

This fee stays the same whether you buy the fund with Betterment or use another investing app.

Currently, there are two different pricing plans:

- Digital – .25 percent and no minimum balance requirement

- Premium – .40 percent and a $100,000 minimum balance requirement

Regardless of the tier, your account balance determines your total fee. If you have over $2 million with Betterment, you receive a .10 percent marginal discount on balances over $2 million.

The main difference between the tiers is that you get unlimited calls with CFPs with the Premium tier. Aside from that, almost every feature is the same. However, you can buy one-time advice calls with the Digital plan if you need expert insight.

Pros and Cons

There is a lot to like about Betterment. However, it’s not a perfect platform.

Pros

- Recommends a goals-based asset allocation

- Invests in cost-efficient stock and bond index funds

- Automatic rebalancing

- Tax-loss harvesting

- Free cash management and checking accounts

- Financial advisor access

- No minimum account balance to open

If you’re a new investor and want to start investing, Betterment simplifies the process. The app creates portfolios based on your goals and makes sure you don’t have to figure out too much on your own. It doesn’t get much simpler than that.

Cons

- Annual account fee

- Tax-coordinated investing doesn’t sync with external accounts

- Cannot manage your own investments

- Unlimited financial planner access is only for Premium plan

While Betterment is the most established player in the robo-advisor space, there are other options worth considering. Here are a few of the top investing apps for beginners.

| Betterment | M1 Finance | Stash |

|---|---|---|

Read Review | Read Review | Read Review |

Beginner-friendly | Commission-free trading | Beginner-friendly |

Completely automated | Automated rebalancing | Easy-to-use mobile app |

No account minimum | $100 account minimum | No account minimum |

12 months commission-free | No signup bonus | $5 signup bonus |

Who is Betterment Best For?

This is a good option for investors of any experience level, including:

- New investors

- Busy parents and professionals

- Long-term investors

- Index fund investors

- Retirees wanting a low-risk bond portfolio

Betterment makes building a goal-based portfolio easy. It’s possible to start investing in a few minutes.

Instead of spending hours researching which funds to buy and creating an asset allocation, Betterment does the hard work for you. You will invest in many of the largest index ETFs.

However, the robo-advisor might not be the best fit for you if you’re comfortable managing your own portfolio. Most investing apps no longer charge trade commissions on ETFs.

This means you can use the same asset allocation and avoid Betterment’s annual fee.

Betterment Review

-

Commissions and Fees

-

Tools

-

Ease of Use

-

Investment Options

-

Customer Service

Betterment Review

Betterment is a leading robo-advisor that offers low-cost advice for investors. If you need assistance in managing your investments and reaching your goals, it’s a good resource to use.

Overall

4.2Pros

✔️ No minimum account balance to open ✔️ Full breadth of tools to manage your investments and cash ✔️ Incredibly affordable to use ✔️ Uses a goals-based approach to manage your investments ✔️ Free tax-loss harvesting

Cons

❌ Minimal options for experienced investors ❌ Can’t include external accounts in your recommendations ❌ Can’t manage your own investments

Summary

Betterment is one of the best options if you want to start investing and need help. Their fees are low, you get a diversified portfolio, and you can invest small amounts of money. As your investing skills grow, you can open a DIY account elsewhere to buy individual stocks or sector ETFs.

Remember, you can open an account with Betterment with no minimum balance.

What challenges are you facing with investing in the stock market? How often do you look at your investment portfolio?

I’m John Schmoll, a former stockbroker, MBA-grad, published finance writer, and founder of Frugal Rules.

As a veteran of the financial services industry, I’ve worked as a mutual fund administrator, banker, and stockbroker and was Series 7 and 63-licensed, but I left all that behind in 2012 to help people learn how to manage their money.

My goal is to help you gain the knowledge you need to become financially independent with personally-tested financial tools and money-saving solutions.

I’ve read a bit about Betterment before, and it sounds like good stuff. More info for Rick and I to consider as we get ready to start investing. Fun and games planned for this weekend, woohoo!

Assuming it’s a good fit for you then it could be a good potential fit Laurie. Like I’ve said in the past, feel free to ask me any questions as you move closer to that Laurie I’d be happy to help. 🙂

I have been with Betterment for over a year. My account has brought in over 12% returns for the year and I think that is good enough for me. It is easy and I like it. They currently hold my Roth IRA. That being said, I will be opening a different brokerage account just to do some individual stock trading focusing around dividend paying stocks.

I seem to remember you mentioning that in the past Grayson. Glad to hear they’ve worked well for you and think it’s great you’ll be looking to add some to that through dividend paying stocks.

I do have a Betterment account and it is as easy as you said. I signed up for the bonus earlier this summer, but have kept the account open just to not pay the trading fees, which can eat up your investment if you aren’t putting in a lot of money. I’ll see after a year how the fees compare with doing the same thing at Vanguard.

That sounds good Kim, glad to hear that it has been easy for you. That said, I’d be inclined to think the fees would likely be better at Vanguard.

I think Betterment is definitely a good choice, though I would still prefer that someone start with one of Vanguard’s target date fund, as long as they can meet the $1k minimum. The fees are slightly lower, though the difference isn’t big enough to get too up in arms about. But overall I think the more services like this that exist, the better.

I think they can be, assuming it’s the right fit for your needs. I’d likely be more inclined to go the Vanguard route if you want something simple, though I do like how Betterment seems to take a lot of the guess work out for the novice investor.

I recently wrote a review of Betterment. It was that review that got me to start investing. I got into Betterment and earned over 9% in 4 months. I’m loving it. This is a great outline too!

I remember seeing that Josh and glad to hear that it got you started investing.

Great review John, and I appreciate you pointing out some of the negatives of Betterment as well as the positives. I am looking to open some investment accounts in the new year, perhaps an IRA and then an individual stock trading account. I definitely appreciate your reviews so far this year on various investment companies, most of which I am looking into currently.

Thanks DC! Yea, each brokerage has their own set of good/bad things and those related to Betterment are a bit unique. Thanks for the feedback on the reviews, that’s my hope. I have a couple more planned over the next few months and will follow it up with a roundup overview afterwards.

I agree that Betterment may be good for beginning investors. I like the pool of funds they use, which are mostly low-cost Vanguard index funds. They use a strategy that is called slice-and-dice where rather than using the market cap-weighted index fund (VTI), they add in some mid and small-cap value index funds. I do some of this on my own without paying Betterment’s additional fees. My only hesitation with recommending Betterment to new or small investors is that people often stay with what they are comfortable with. That would not be all that bad with Betterment, but people would make more money by eventually handling their investments themselves. Personally, though, I would rather just give a new investor a copy of the Bogleheads’ Guide to Investing, let them read it, and then help them set up a portfolio.

I like their pool of funds and do that on my own as it is. That is a good point about new investors staying with what they’re comfortable with and can really hinder them in the long run if they stay with that mindset.

I see your point on what you’d recommend, the problem is though that the large majority of new investors out there can’t do that effectively. I spoke with people in that spot every day for several years and even that was advanced for them.

I’ve been torn between using a service like Betterment or WealthFront, or a traditional financial advisor, but am kind of terrified by the giant upfront fees and the research to suggest that index funds outperform managed funds over the long run.

And then reading that the Vanguard funds have even lower fees. So still not sure what to do.

In fact, the indecision has led to sitting on the sideline for most of the year and missing a nice 25% run up!

I’ve not heard much about WealthFront, so I couldn’t answer to that. I can understand not wanting the fees of a traditional advisor though.

Sorry to hear you’ve missed out of the run up. That said, you generally can’t go wrong with a solid, low-cost index fund especially if you’re undecided on where to put your money in the market.

I just can’t seem to wrap my head around their fee structure, which is really kind of high (considering most accounts will likely have less than 100k), compared to a vanguard index fund. Do they use some sort of algorithm based on answers to questions, or is it personalized service?

From what I’ve read and researched it’s not algo based, but it personalized to you. That said, I could certainly be wrong on that. What you have to remember about the pricing though is that you’re paying nothing for the trading, rebalancing, etc. It may not be cheaper than a Vanguard fund, but you’d be surprised at how many have difficulties deciding on a Vanguard fund.

Sounds like a solid approach. However, this is really just another wrapper around a diversified portfolio of index funds. Look, you can go to Fidelity, Schwab or Vanguard and get pretty much the same thing. They have detailed questionnaires to judge risk tolerance and you sit down with them to craft a portfolio of diversified no-load mutual funds, index funds and ETFs. You do a mix of large, medium and small funds that cover growth, value and blend and you can get a fairly close result with less cost.

I think it is for the right investor Steven. That said, yes many can go the route of Fidelity, Vanguard and the like but many would not even qualify to have that ability to sit down and talk with someone about the right kind of portfolio to set up for themselves because of the amount they’d be starting with. In the end, it’s another option for a beginning investor to consider as they need to make sure they find something that fits what they need and are comfortable with.

I keep seeing comments that Betterment is good for beginners. But is it good for someone who’s been investing but is not the DIY type. I’ve been investing for over 10 years, however I have not been active with my accounts. I’ve gone with an advisor and bought some mutual funds that they recommended and it’s just sitting there. I just came to realize how much I’m paying in fees and wanted to look at reinvesting somewhere else. I want something simple but will still get me to my retirement goal. I don’t mind paying a little bit of fees to not have to worry about researching who to invest with and opening accounts with multiple brokerage firms. I also like the automatic rebalancing and tax loss harvest. Would you say this is good for someone like me? I am concerned about the self-custodian part…is my money safe? Is the gains they say accurate?

Thanks for stopping by Cindy! Not knowing your exact situation, it can be hard to say with definitive confidence that it would be good for you. That said, if you are looking for a more hands off approach that will do much of the heavy lifting for you then Betterment could be a decent option. The fact that they take care of much of the ins and outs is something that’s attractive to me as you don’t really have to deal with it day in and day out as well as having a ton of fees as a result.

In terms of protection of your money…with Betterment being a brokerage you’re covered through SIPC insurance, which is the brokerage cousin to the FDIC. With SIPC, you’re covered up to $500,000 in account value, of which $100,000 can be cash. What SIPC essentially covers is if the brokerage goes belly up your principle is covered to that amount, though not any losses you may have incurred in the market. Short story long, you’re money would be covered up to that $500,000 threshold. 🙂

How about safety with this new company? To my understanding the SPIC insurance didn’t help many of the Stanford, the Madoff, or the Morales victims. Where are the assets held? How safe are these people?

All great questions Marie! I can’t really speak much to the other victims, but I’ve read quite a bit that some of the Madoff victims were repaid by SIPC, though maybe not completely. The question, as I understand it, is whether or not they were direct investors of Madoff or if they came in indirectly.

At any rate, in relation to Betterment, personal assets at Betterment are held in street name. Meaning, they’re separate from any other assets at Betterment and are not used to be loaned out (as in the case of a margin account). They do offer the standard SIPC coverage – $100k cash & $400k securities and they’re a custodial just like someone like Schwab or Fidelity where they’re required to keep all records of your assets.

I hope that helps and please let me know if there is anything else I can answer in relation to this. Thanks for stopping by. 🙂

Hello, I am a college student therefore have a tight budget. However, I am very interested in investing my money to start accumulating capital in order to start my own business in the future. It seems as though Betterment might be a good fit for me as a beginner investor. I would be able to withdrawal between $25-$50 a month from my checking account. What would be a realistic goal on my returns? Is there anything else I should know before opening an account with Betterment?

Good questions Mehdi. The first question I’d ask is how much control are you wanting to have over the investing? Are you essentially wanting someone to manage it for you – or are you wanting to make the decisions on what specific investments you’ll be in?

If it’s the former then Betterment is going to be the best option out there. I’d recommend Wealthfront, but they have a minimum balance requirement of $5,000. Betterment does not have that. If it’s the latter, I’d likely go with someone like Motif Investing which gives you a good mix of each. Here’s my review of them –

https://www.frugalrules.com/motif-investing-review-investing/

As to the return capability, there’s no real way of saying that as no one knows what the market will do. That said, Betterment does take a good basic approach of following the market as opposed to chasing gains.

Hope that helps! 🙂 Feel free to let me know if you have any other questions.

Hello guys, the comments you all made really helped me to understand some things about investing witch I want to do. I don’t have a lot to invest and I am surely a beginner. I want to understand how little I can invest. If I understand correctly, at betterment I can invest as little as a $100.00 a month. Is that correct? If so what can I expect in return in the long term haul?

Glad you’ve found it helpful Keith and awesome you want to get started investing! Yes, you are correct, Betterment allows you to start with as little as $100 per month.

There’s no way to say how it’d perform in the long-term unfortunately. That being said, their approach is one that aims to be passive and stay with the market – and not something crazy like trying to time the market. That approach will generally help your holdings perform the way the market as a whole is. Hope that helps & thanks for stopping by.

i like the reviews of the betterment and thought this was a great break down. but if you start out with just 100$ a month and they are taking 35% of that each month are you really going to make any money? if nearly ever deposit is hit for almost half? guess i am a little confused.

Thanks Timothy! Thank you for stopping by as well. The fee is actually .35% of your annual balance if you make the $100/mo deposit – so not truly $35 out of each $100 you deposit . If you’re under that amount per month they move you to the .25% annually plus $3/month.

One other option to look at is Wealthfront – here’s a review I did of them – https://www.frugalrules.com/wealthfront-review/

They have a minimum balance to start of $500, but you get the first $15k managed for free then .25% annually. They don’t require a monthly deposit like Betterment does. They operate very similar to Betterment and offer many of the same funds. Hope that helps, happy to answer any other questions.

I really like Betterment and had great success with it. I think that tax loss harvesting alone makes me forget the fees. It is definitively a great choice for non-registered accounts.